FinTech

Best 5 Low Interest Loans in Malaysia (2025 Edition)

If you’re reading this, chances are you’re either planning a big move—like renovating your home—or maybe you just need a bit of financial breathing room. Either way, finding a low interest personal loan in Malaysia can make a big difference in how comfortably you can manage repayments.

After spending a solid few days comparing the options on sites like RinggitPlus and going through the fine print, I’ve put together this 2025 guide to help you choose the right personal loan Malaysia offers—one that’s low in interest, but high in value.

Why Choosing a Low Interest Loan Matters

Let’s be honest—borrowing money is easy. But the moment repayment starts, reality kicks in. That’s why we do recommend you to do some in depth research before applying for the best personal loan in Malaysia for you. When you start to look into it, that’s where the loan interest rate makes all the difference. A few percentage points might not sound like much, but over 5 to 7 years, it could mean saving thousands of ringgit.

I learned this the hard way when I first took out a loan at 7% thinking it was “reasonable” within the market of low interest loans. Spoiler: it wasn’t.

Quick Comparison: Lowest Interest Personal Loans in Malaysia (2025)

| Lender | Flat Rate (p.a.) | Loan Range | Tenure | RM5k for 5 years (Est.) |

| UOB Personal Loan | From 3.99% | RM5k–150k | Up to 5 years | RM92/month |

| Alliance CashFirst | 4.99% + cashback | RM5k–200k | Up to 7 years | RM95/month + cashback |

| CIMB Cash Plus | From 4.38% flat | RM5k–100k | Up to 5 years | RM91/month (flat, ~8% EIR) |

| HSBC Amanah-i | From 4.88% profit | RM6k–250k | Up to 7 years | RM96/month |

| Bank Islam Financing-i | From 4.50% profit | RM10k–300k | Up to 10 years | RM94/month |

These aren’t just attractive numbers—they’re real, from verified lender sources, and worth exploring.

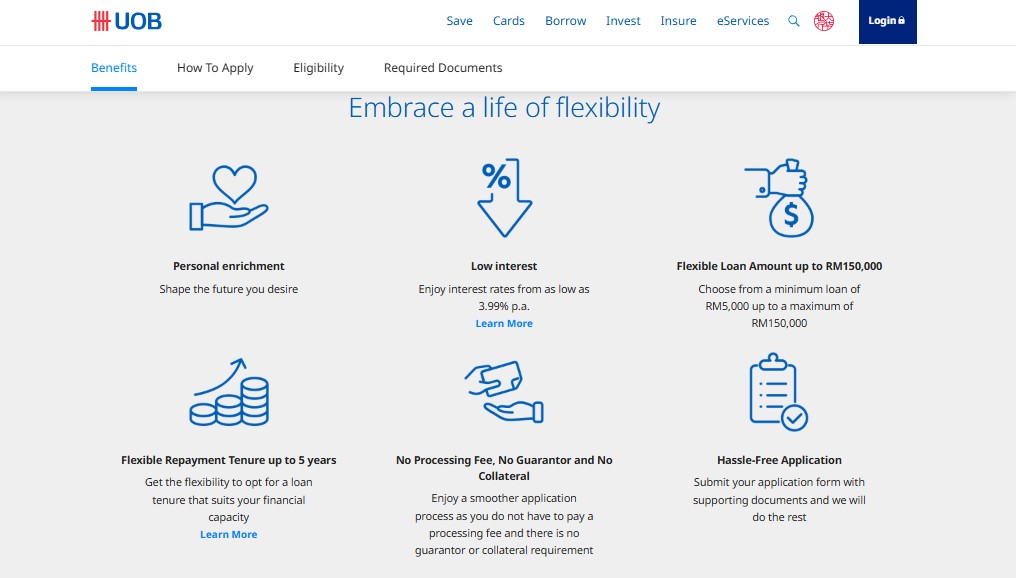

1. UOB Personal Loan – Best Flat Rate on the Market

Interest rate: UOB consistently offers the lowest flat rate for personal loans in Malaysia—starting at 3.99% p.a.

Real case: I helped a friend to apply in January. Online application was smooth, with the funds disbursed within 48 hours. Minimal fuss, and no weird conditions buried in the fine print.Most importantly, the low interest loan with the best rate within the market.

Ideal for: Anyone who’s clear on the repayment period and prefers a simple, straightforward deal.

2. Alliance Bank CashFirst – Cashback That Actually Works

Interest rate: Flat 4.99% p.a.

Standout feature: You get cashback up to 30% on the interest paid, making it one of the most rewarding loans if you hold it full term.

Real case: My cousin borrowed RM30,000 over five years and got about RM2,200 back. It’s like earning money for borrowing responsibly.

Ideal for: Borrowers who want a mid-to-long term low interest loan with a little bonus at the end.

3. CIMB Cash Plus – Fast, Simple, Transparent

Interest rate: From 4.38%, but effective interest rate (EIR) can be around 8%.

Standout feature: Zero fees for processing or early settlement. Instant approval (mine came in 10 minutes).

p/s: Flat rates look low, but make sure you understand the EIR—it’s what really affects your total repayment.

4. HSBC Amanah Financing-i – Shariah-Compliant, No Hassles

Profit rate: Starting from 4.88%.

Standout feature: It’s Shariah-compliant, so there’s no compounding interest—just profit-sharing. You know exactly what you’re paying. No need for guarantors or collateral.

Ideal for: Muslims looking for ethical financing that aligns with religious values. Also great for anyone who appreciates clarity.

5. Bank Islam Personal Financing-i – Flexibility Above All

Profit rate: From 4.50%.

Standout feature: Offers up to 10 years repayment, giving borrowers room to breathe.

Ideal for: Large low interest loans like education, home upgrades, or even business expansion where lower monthly repayments are key.

p/s: You’ll pay more interest over time—but it can be worth it if your cash flow is tight.

🔍 Flat vs Effective Rate: What’s the Catch?

Let’s say you take a flat rate of 4.38%. You think it’s a steal. But that flat rate only applies to the original amount borrowed, not the reducing balance.

👉 So the EIR—which considers how much of the loan is left over time—might actually be closer to 8%.

Pro tip: Always ask for the effective interest rate. It’s the more accurate picture of what you’ll pay.

🧠 Insider Tips for First-Time Borrowers

- Don’t judge by rate alone. Cashback and zero-fee early settlements can make a higher rate cheaper overall. So don’t just focus on low interest loans, check out their promotional perks as well.

- Use a loan calculator. Play with tenures and amounts to find your monthly sweet spot.

- Go for shorter tenures if you can afford it. Less total interest, faster payoff.

- Refinancing is an option. Started with a fast loan? You can switch later to a better long-term rate.

📌My Experience

I once needed RM50,000 to cover unexpected medical costs.

- I compared UOB and Bank Islam.

- UOB offered 3.99% flat—monthly instalment of RM476.

- Bank Islam gave me a 10-year plan with 4.50% profit—monthly RM518 but longer repayment.

In the end, I chose UOB for lower interest, but the shorter tenure meant I had to budget more aggressively. If you need more flexibility, the Islamic plans definitely offer room to breathe.

🎯 Takeaway: Which Loan Is Right for You?

- Lowest rate? ➤ UOB

- Extra perks? ➤ Alliance Bank

- Fast & simple? ➤ CIMB Cash Plus

- Islamic option? ➤ HSBC Amanah or Bank Islam

- Longest tenure? ➤ Bank Islam

In the end, a low interest personal loan isn’t just about getting the “cheapest” deal—it’s about finding one that fits your lifestyle, repayment ability, and long-term goals.

Borrow smart. Your future self will thank you.

🤔 FAQ: Low Interest Loans in Malaysia 2025

Q: Which personal loan has the lowest flat rate?

A: UOB currently leads with 3.99% flat.

Q: Are Islamic loans really cheaper?

A: Not always, but they’re more transparent and may have fewer fees.

Q: Can I apply online?

A: Yes—all five banks listed offer online or mobile-first application options.

Q: Is there a catch with cashback loans?

A: Usually not—but you’ll only get the full cashback if you don’t miss any payments.

Q: How fast is approval?

A: Typically 1–3 working days. Some banks, like CIMB, offer instant approval.

RTX 4070 Super AIB Review: Thermals, Noise, Performance

Best Streaming Webcams 2025: 4K & 60fps Picks for Creators

Why Singapore and the UAE Are Setting the Benchmark in Global Crypto Innovation

Why Contractors Are Turning to Smarter Tools to Keep Projects on Track

Digital Payments and How They are Changing Online Gaming in Malaysia

Employer of Record Brazil: Build Global Teams with Confidence

Common Challenges in Solana Token Development and How to Overcome

Input Lag and Touch Targets – Tiny Details, Big Feel on Mobile

Understanding Hydrocodone Withdrawal Symptoms and Treatment